Retirees Actually Spend Less in Retirement—Two New Studies Show JP Morgan and Transamerica released retirement studies that included data on how much retirees actually spend vs. what they thought they would spend. The conclusion, surprisingly, is that many people spend LESS than what they thought they would spend. To download both of these studies, click on the following: www.uploadedimages.net/content/PDFs/two-retirees-spend-less-studies.pdf The studies may give consumers reason to rethink how much they will spend in retirement (and for many this will be a relief if they have not saved enough to reach their retirement goals). JP Morgan—this study looked at more than 280,000 households (a huge number) and here are some highlights from the study: -More than half of the households (couples) did not retire all at once (one spouse retired early or one spouse continued to work part-time).

–Partially retired households tend to spend MORE than their fully retired peers.

-Many households who had less than $150k pre-retirement income had a spending splurge in the few years after retirement.

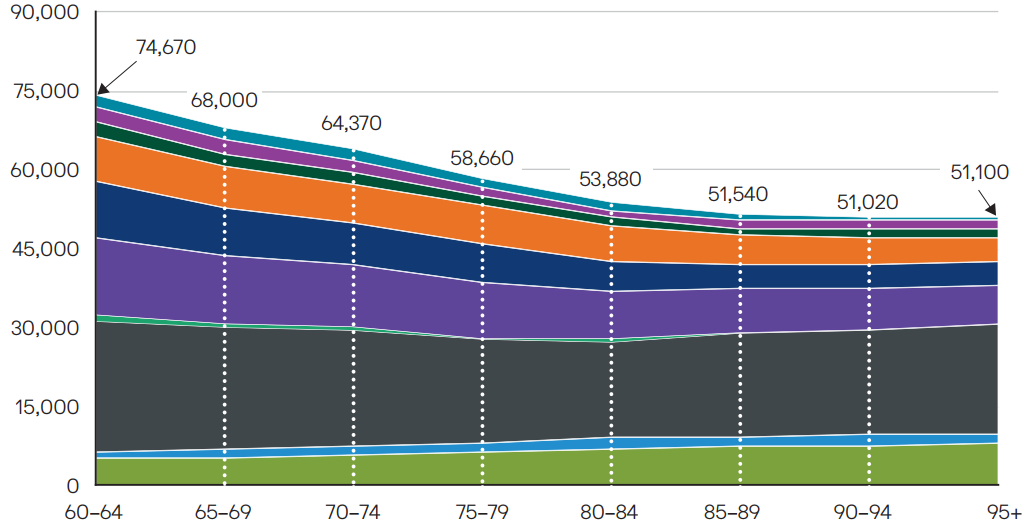

-Older households (65+) spend more on health care and charitable gifts, but SIGNIFICANTLY LESS on everything else. The following chart is what got my attention. See the downward trend in spending.

|

Transamerica—this study is of those already retired. The key takeaway for this newsletter is that 50% of those surveyed said their expenses since retiring have DECREASED!

This study is 77 pages long. It has a lot of interesting info such as: -Top retirement priorities

-How life has changed since retiring

-Caregiving experience (like caring for parents, spouses, other family members or friends)

-Actual retirement age

-Did you retire sooner, later, or at the expected age (most retired sooner)

-Retirement confidence

-Financial priorities (paying off debt was #1)

-Age you started Social Security Benefits (median age is 63)

-Greatest retirement fears Both of these studies have a lot of useful information and are ones consumers can use to better understand how much money may actually be needed in retirement. Want Help Building Your Retirement Plan? While these studies indicate that many people will actually spend less in retirement, that doesn’t help consumers determine if they are on track to retire with enough money. One expense that is overlooked by consumers and the advisors who give them advice is Medicare. Most people when they turn 65 will apply for Medicare to be their primary health insurance carrier. The following are the projected cost increases from the Medicare Trust Fund report.

Medicare Part B: -2025–2033: Projected average annual increase = 8.2%

–2034–2048: Projected average annual increase = 5.5%

-2049–2098: Projected average annual increase = 4.2%

The projected baseline per person Medicare premium (using an 8.2% increase) in 2033 = $4,999 per year/per spouse. That’s nearly $10,000 in expenses for a couple in 2033 that most consumers and their advisors are NOT planning for. If your MAGI (Modified Adjusted Gross Income) is high enough, you will be subject to an increased premium (what they call the Income-Related Monthly Adjustment Amount (IRMAA penalty). That penalty can increase Medicare premiums by over 300%. If you would like our firm to build for you a REALISTIC retirement plan that takes into account all the important variables so you can determine if you are on track to meet your retirement goals, please contact us.